Inflation . What is it?

Inflation is a tool of the capitalist. Or just a random thing that happens in a complex system of interacting…h.hh.t.yt,6u… Read More Inflation . What is it?

Inflation is a tool of the capitalist. Or just a random thing that happens in a complex system of interacting…h.hh.t.yt,6u… Read More Inflation . What is it?

The decentralised/blockchain community holds independence, freedom and a lack of hierarchy as a core ideal, however they are using a flawed method from game theory that will do the opposite of their intentions. Staking Staking is everywhere in the new decentralised economy. Whether it be Proof-of-Stake to determine who gets to verify a transaction –… Read More The problem with staking in the decentralised world

There is no reason to have a lender when you borrow money, you can just borrow from yourself at zero interest. How is this possible? Our view of money and debt has changed significantly in the last 12 years since the GFC. We used to think banks took our deposits of government printed cash and… Read More Lender-less borrowing – the end of banks

Abstract Fluid Democratia is a fully integrated decentralised socio/economic system based on a decentralised ledger. It incorporates a new currency, universal income, P2P lending, currency exchange, Land registry, and liquid democratic resources and infrastructure management. The purpose is to create a parallel system to the current hierarchical organisational structure. The aim is true freedom with… Read More Fluid Democratia – decentralised society

I ask this question in part because of my recent experience with crowd funding, the idea behind crowd funding is to support some ones idea, project, or invention by giving them some money. They may promise to give a gift in return but there is no contractual agreement to provide a product or service in return… Read More Is giving a gift more morally decent than contracting an exchange?

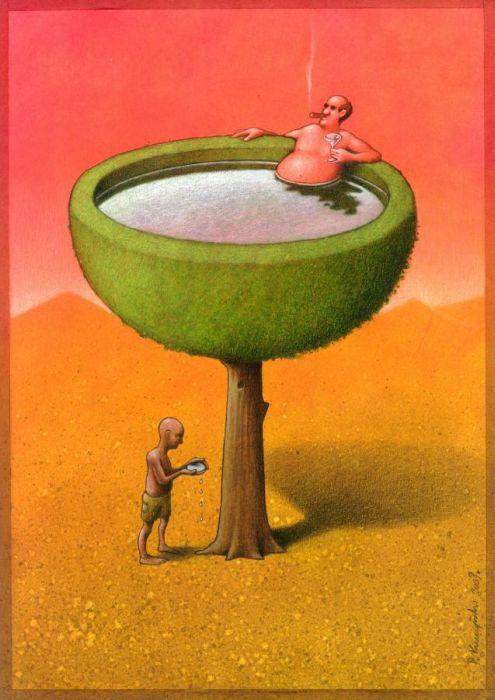

Luck determines the winners and losers of society, not merit or hard work. Those that start out with more get more, and those that start with little often fall through the gaps. Inequality is not only caused by the human inventions of rent, profit and interest but also by a quirk of the economic… Read More Why the rich get richer and the poor poorer

There’s been a lot of chatter in the media recently about AI (Artificial Intelligence), mechanisation, and driverless cars taking all our jobs. I’ve heard this before in the 80’s but it didn’t happen. Why? There is new evidence everyday that human labour is just not necessary anymore. Adidas has created its first fully mechanised… Read More Computers are taking our jobs – again

Elected governments really don’t have much power any more because they have ceded most of it to corporations which we believe we control through share ownership but we are hopelessly wrong. Corporations are some of the few organisations that have true global influence so if we were to have a global democracy we would want… Read More The fallacy of Shareholder democracy – the owners are all opaque holding companies

[cs_section id=”” class=” ” style=”margin: 0px; padding: 45px 0px; ” visibility=”” parallax=”false”][cs_row id=”” class=” ” style=”margin: 0px auto; padding: 0px; ” visibility=”” inner_container=”true” marginless_columns=”false” bg_color=””][cs_column id=”” class=”” style=”padding: 0px; ” bg_color=”” fade=”false” fade_animation=”in” fade_animation_offset=”45px” fade_duration=”750″ type=”1/1″][x_custom_headline level=”h2″ looks_like=”h3″ accent=”false”]Banks do create credit from nothing but they need to get the money back again to balance… Read More Banks do create money from thin air